Why Higher Unit Prices Don't Earn Better Payment Terms Below MOQ

When procurement teams negotiate orders below the minimum order quantity for custom tech accessories, a common assumption surfaces: if we're willing to accept a higher unit price, the supplier should offer more flexible payment terms. This expectation feels reasonable—after all, the elevated pricing should compensate for the inconvenience of a smaller batch. Yet in practice, buyers ordering 80 branded power banks at $42 per unit consistently face stricter payment conditions than those ordering 300 units at $36 per unit, despite paying 17% more per piece.

The disconnect stems from a fundamental misunderstanding of how suppliers assess financial risk. Unit pricing and payment terms operate in separate risk frameworks. While unit price reflects production economics—setup costs, material efficiency, and throughput—payment terms are determined by absolute dollar exposure, relationship history, and default probability. A supplier evaluating whether to extend credit doesn't calculate risk based on margin per unit; they calculate it based on total capital at stake if the buyer fails to pay or cancels mid-production.

Consider a typical scenario in the Malaysian custom electronics market. A corporate client approaches a manufacturer for 75 custom Bluetooth speakers with logo engraving. The supplier quotes $45 per unit—a 25% premium over the standard 200-unit MOQ price of $36. The buyer, having accepted this premium, expects payment terms similar to larger orders: perhaps a 30% deposit with the balance payable 30 days after shipment. Instead, the supplier requests 60% upfront and the remaining 40% before goods leave the factory. No credit period. No flexibility.

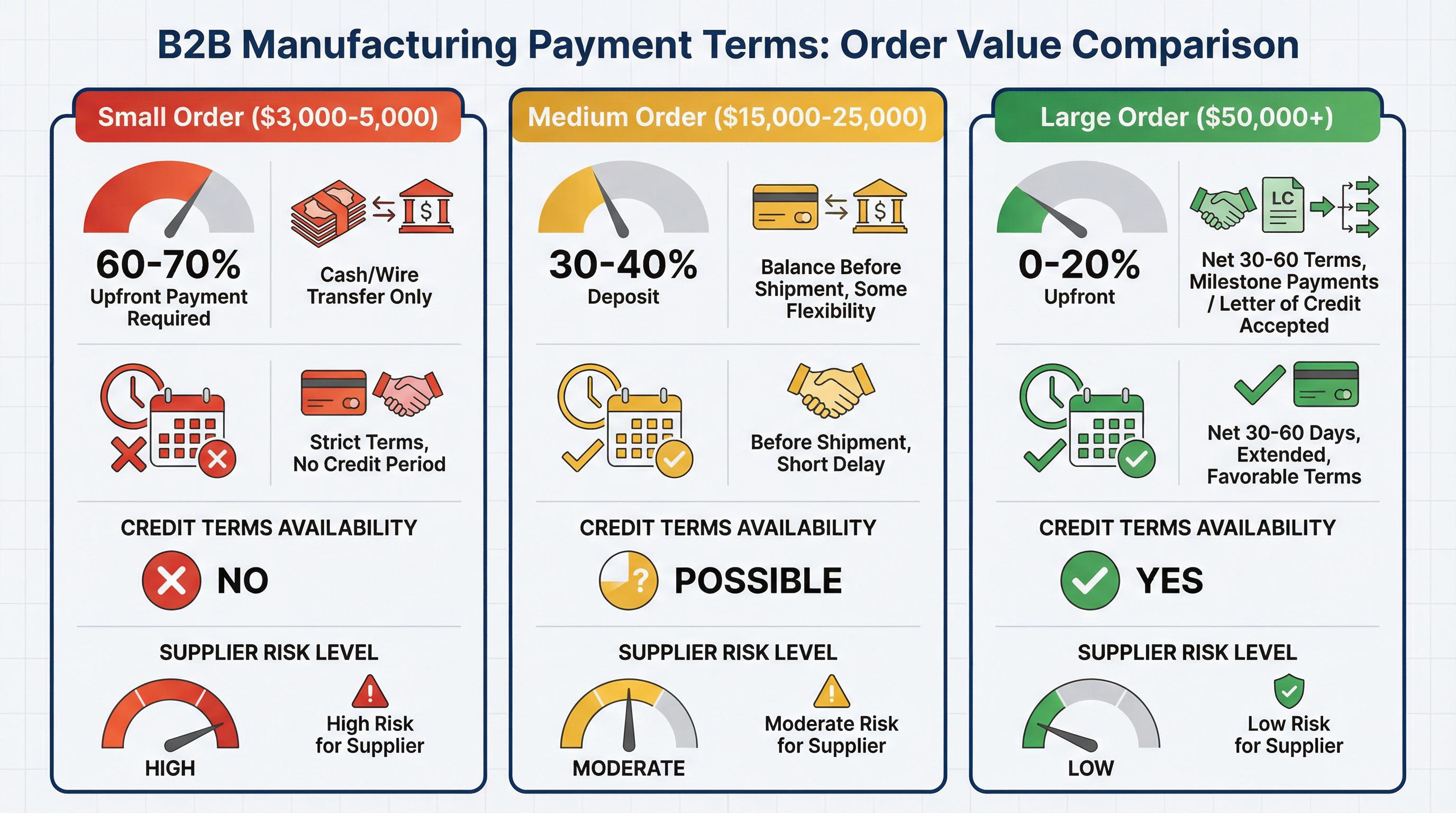

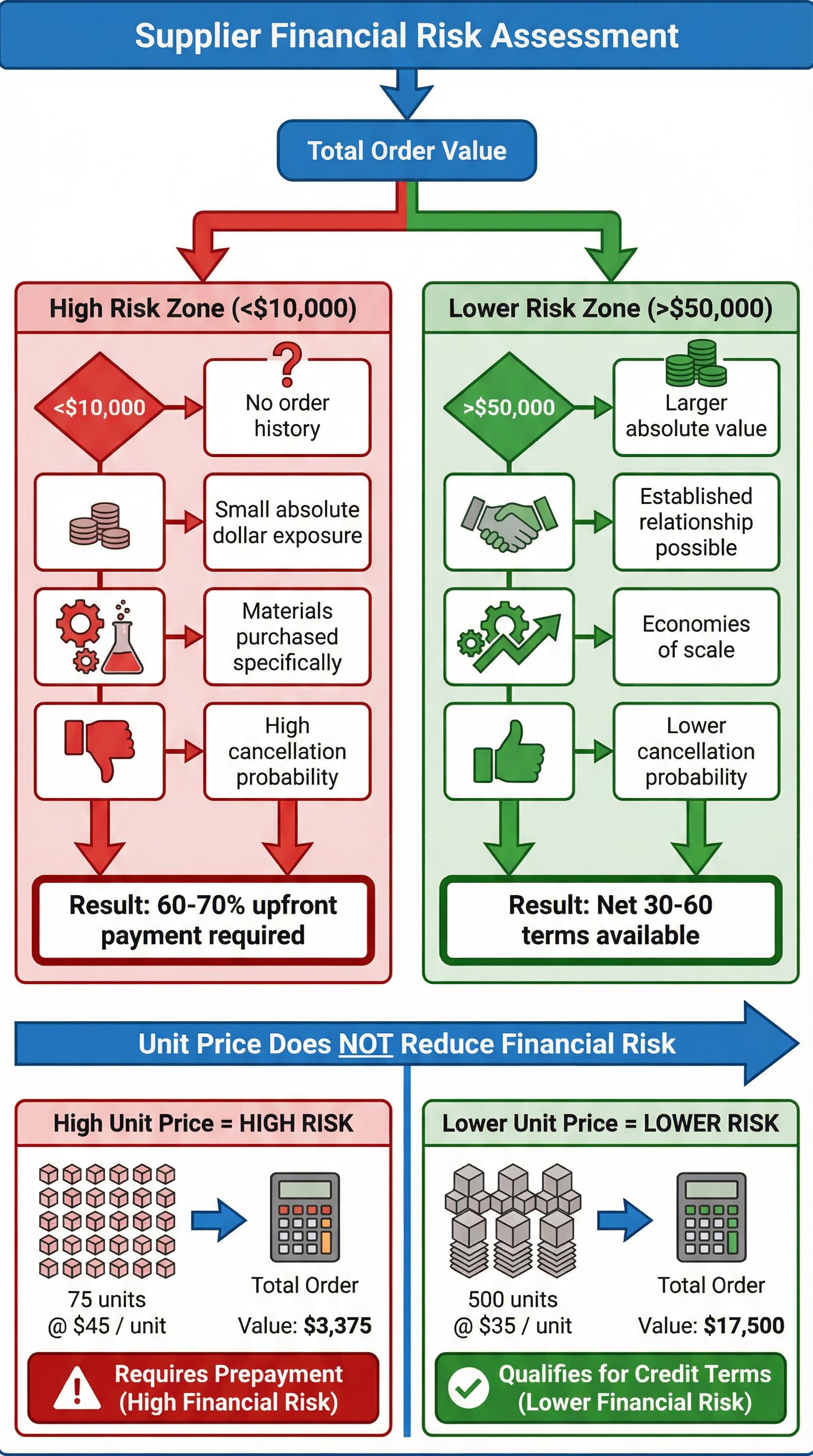

The buyer's frustration is understandable but misplaced. The supplier's payment structure isn't arbitrary—it's a direct response to the order's financial profile. At $45 per unit for 75 pieces, the total order value is $3,375. From the supplier's perspective, this represents a high-risk, low-value transaction. The absolute dollar amount is too small to justify extending credit, regardless of how profitable each individual unit might be. Industry data confirms this pattern: orders under $10,000 typically require 50-70% upfront payment, while orders exceeding $50,000 often qualify for Net 30 to Net 60 terms. The threshold isn't about unit economics—it's about total exposure.

This risk calculation becomes clearer when examining what happens if a buyer defaults. For a $3,375 order, the supplier has likely purchased materials specifically for this batch—custom PCB panels, specific color injection molding compounds, laser-etched packaging. These components have limited reusability. If the buyer cancels after production begins or fails to make final payment, the supplier's recovery options are severely constrained. They cannot easily redirect these customized materials to another client. The small order value also makes legal collection impractical; pursuing $1,350 (the 40% balance) through formal channels would cost more than the debt itself.

Contrast this with a 500-unit order at $35 per unit, totaling $17,500. Despite the lower unit price, this order presents lower financial risk. The larger absolute value justifies the administrative overhead of credit management. The supplier can implement milestone payments—30% deposit, 40% at production completion, 30% within 30 days of shipment. If the buyer defaults on the final payment, the $5,250 outstanding balance is substantial enough to warrant collection efforts. More importantly, the economies of scale in a 500-unit run mean materials are purchased in standard quantities that can be partially reallocated if needed.

The relationship between order value and payment terms follows a clear hierarchy. First-time buyers placing orders under $5,000 face the strictest conditions: typically 50-70% deposit with full balance due before shipment. There is no credit period, no payment flexibility, and often no negotiation room. Orders between $10,000 and $25,000 from established clients might secure 30-40% deposits with balance before shipment, representing a modest improvement but still no post-delivery credit. Only when orders exceed $50,000—or when a buyer has completed multiple successful transactions—do suppliers consider Net 30 or Net 60 terms. At this tier, letters of credit become viable, milestone payments are negotiable, and the relationship shifts from transactional to partnership-based.

The practical implications of this payment structure create cash flow challenges that many procurement teams underestimate. A buyer ordering 80 custom USB drives at $38 per unit ($3,040 total) must typically pay $1,824 to $2,128 upfront (60-70%), with the balance due before shipment. This means the full $3,040 is committed before the buyer receives or inspects the goods. For a larger order of 400 units at $32 per unit ($12,800 total), an established client might pay $3,840 upfront (30%) and $8,960 within 30 days of delivery. The larger order, despite being four times the dollar value, requires less immediate cash outlay as a percentage and provides a credit window for inspection and resale.

This payment timing becomes critical when buyers are ordering custom tech accessories for specific events or promotional campaigns. The 80-unit order requires full payment potentially 6-8 weeks before delivery (deposit at order placement, balance at production completion). If quality issues emerge or specifications are incorrect, the buyer has already committed 100% of funds with limited recourse. The 400-unit order, with its post-delivery payment component, provides a buffer for quality verification and gives the buyer leverage if problems arise.

Suppliers justify these stricter terms through a multi-factor risk assessment that procurement teams rarely see. For orders under $10,000, suppliers evaluate: (1) the absence of order history, which provides no behavioral data on payment reliability; (2) the small absolute dollar exposure, which makes credit administration costs disproportionate; (3) the purchase of materials specifically for this order, which cannot be easily repurposed; and (4) the statistically higher cancellation probability for small, experimental orders. Each factor independently argues for prepayment; combined, they make credit extension financially irrational from the supplier's perspective.

The unit price premium that buyers pay for small batches addresses a completely different cost structure. That $45 per unit for 75 Bluetooth speakers versus $36 for 200 units reflects setup cost amortization, production line efficiency losses, and material purchasing disadvantages. The supplier is compensating for the fact that die-cutting setup takes the same 45 minutes whether producing 75 or 200 units, that a production line running at 60% capacity has the same fixed costs as one at 90%, and that buying 80 meters of custom fabric costs more per meter than buying 250 meters. These are operational costs, not financial risks.

Payment terms, by contrast, address capital risk and administrative burden. When a supplier extends Net 30 terms, they are providing working capital financing—essentially a 30-day interest-free loan. For a $17,500 order, this might represent $5,250 in outstanding receivables (assuming 30% upfront). The supplier must assess: Can we afford to have $5,250 tied up for 30 days? What is the probability this buyer will pay on time? What are our collection options if they don't? For a $3,375 order, even if the supplier were willing to extend similar terms, the $1,012 in outstanding receivables (30% of total) doesn't justify the credit management infrastructure—credit checks, payment tracking, collection procedures—required to manage it.

This separation of pricing and payment risk explains why buyers cannot "buy their way into" better payment terms through higher unit prices. A buyer offering to pay $48 instead of $45 per unit for those 75 Bluetooth speakers—a 6.7% price increase—does not reduce the supplier's financial risk. The total order value rises from $3,375 to $3,600, but this $225 difference doesn't change the risk profile. The order is still below the $10,000 threshold where credit terms become viable. The supplier still faces the same default risk, the same material commitment, and the same collection challenges. The additional $225 in revenue doesn't offset the potential loss of $1,440 (40% balance) if the buyer defaults after production.

The industry's payment term thresholds have evolved through decades of supplier experience with default rates and collection costs. Data from B2B payment platforms shows that orders under $10,000 have default rates 3-4 times higher than orders over $50,000. This isn't because smaller buyers are less trustworthy; it's because smaller orders are more likely to be experimental, tied to uncertain demand, or placed by newer businesses with less stable cash flow. The higher default rate, combined with the disproportionate cost of collecting small debts, makes prepayment the only economically rational approach for suppliers.

Buyers sometimes attempt to negotiate better payment terms by offering to establish a long-term relationship or commit to future orders. While relationship building does eventually improve payment terms, suppliers require demonstrated payment behavior before extending credit. A typical progression might see a first-time buyer face 60% deposit terms, then after two successful orders move to 40% deposit terms, and only after six orders qualify for Net 30 terms—assuming order values have grown above $15,000. The supplier needs evidence that the buyer pays on time, doesn't cancel orders, and represents stable ongoing business. Promises of future volume don't reduce current risk.

The payment term structure also reflects the supplier's own cash flow constraints. Manufacturers of custom tech accessories operate on thin margins, typically 8-15% net profit. For a supplier with $500,000 in monthly revenue, extending credit on multiple small orders quickly creates cash flow stress. If they have ten clients each owing $3,000-5,000 on Net 30 terms, that's $30,000-50,000 in outstanding receivables—10% of monthly revenue tied up in credit. For small and medium-sized manufacturers, this capital constraint makes prepayment requirements a survival necessity, not a negotiating position.

The disconnect between buyer expectations and supplier reality often surfaces during payment term negotiations. Buyers present the higher unit price as justification for flexibility: "We're paying $9 more per unit than your MOQ price—surely that earns us standard payment terms." Suppliers respond by pointing to the total order value: "Your order is $3,600. We extend credit starting at $15,000 for established clients, $25,000 for new clients." The conversation reaches an impasse because the parties are measuring risk in different units—one in price per piece, the other in total dollars at stake.

This fundamental mismatch in risk perception creates friction that damages supplier relationships. Buyers feel they're being treated unfairly despite paying premium prices. Suppliers feel buyers don't understand the financial realities of manufacturing. The solution requires buyers to recognize that payment terms and unit pricing are separate negotiations governed by different risk factors. Accepting a higher unit price doesn't earn credit terms; building order history, increasing order values, and demonstrating payment reliability does.

For procurement teams managing budgets for custom tech accessories, this payment structure demands different financial planning. Small-batch orders require full cash commitment upfront, which means buyers need working capital equal to 100% of order value 6-8 weeks before goods arrive. This is fundamentally different from larger orders where 30-40% upfront payment and post-delivery credit terms allow buyers to receive goods, verify quality, and potentially generate revenue before final payment is due. The cash flow impact of small-batch procurement is often more significant than the unit price premium itself.

The strategic implication is that buyers cannot treat payment terms as a negotiable variable when ordering below MOQ. Unlike unit price, delivery time, or specification details—all of which have some flexibility—payment terms are largely fixed by order value and relationship status. A buyer wanting better payment terms has three options: increase order size above the supplier's credit threshold (typically $15,000-25,000), build a payment history through multiple successful small orders, or accept the prepayment structure as a cost of small-batch procurement. Attempting to negotiate credit terms for a $3,000-5,000 first-time order is unlikely to succeed and may signal to the supplier that the buyer doesn't understand manufacturing economics.

The payment term structure in custom tech accessories manufacturing reflects a broader principle in B2B transactions: financial risk is assessed in absolute terms, not relative ones. A supplier doesn't calculate risk as "dollars per unit" or "margin percentage"—they calculate it as "total dollars I might lose if this buyer defaults." This absolute dollar framework means that no amount of unit price premium can compensate for the inherent risk of a small total order value. The buyer paying $45 per unit for 75 pieces is in a fundamentally different risk category than the buyer paying $35 per unit for 500 pieces, regardless of the margin the supplier earns on each unit.

Understanding this distinction allows procurement teams to make more informed decisions about when to order below MOQ. If cash flow constraints make 60-70% upfront payment difficult, the true cost of small-batch ordering may be prohibitive regardless of unit price. If the buyer needs post-delivery credit terms to manage their own cash flow—perhaps because they're reselling the products or need time to verify quality before payment—then ordering below MOQ may not be viable even if the unit price premium is acceptable. The payment term structure, not the unit price, becomes the binding constraint.

The path to better payment terms is clear but requires patience and strategic order planning. Buyers should view their first small-batch order as an investment in supplier relationship building, accepting strict prepayment terms as the entry cost. The second and third orders, if paid promptly and without disputes, begin to establish payment credibility. By the fourth or fifth order, if order values have grown toward $10,000-15,000, buyers can reasonably request modest improvements—perhaps 50% deposit instead of 60%, or balance due 7 days after shipment instead of before shipment. Meaningful credit terms (Net 30 or better) typically require both demonstrated payment history and order values exceeding $20,000-25,000.

The fundamental lesson for procurement teams is that unit price and payment terms operate in separate risk frameworks. Paying a premium for small-batch production addresses operational costs but doesn't reduce financial risk. Suppliers assess payment terms based on total order value, relationship history, and their own cash flow constraints—factors largely independent of per-unit pricing. Buyers expecting that a higher unit price will earn them flexible payment terms are applying the wrong mental model to the negotiation. The supplier has already priced in their operational costs through the unit price premium; payment terms remain governed by financial risk assessment, where small orders face structural disadvantages that pricing cannot overcome.